Meeting new market requirements to Life Sciences & Healthcare distribution in Latin America

Latin America (LATAM) is an important region for Life Sciences & Healthcare (LSH) companies; opportunities include a fast ageing population and a burgeoning middle class to name just two. However, in its current shape distribution in LATAM will become challenging due to changes in the industry, such as personalized medicine and direct-to-patient shipments.

In this article, I want to give an overview of the current situation and explain how LSH companies operating in LATAM can successfully optimize their distribution network to reduce complexity and improve their service offerings.

LSH supply chains are complex; they span pharmaceuticals, generics and medical devices, which have very different needs. In addition to this, the growing focus on delivering pharmaceuticals and medical devices direct to patients adds a layer of complexity previously not seen before – albeit one with great potential and growth opportunities if it can be done successfully.

Further challenges for distribution in LATAM are:

• Demographics e.g. the availability of skilled labor

• Regulations e.g. complex tax codes

• Political complexity e.g. changing political majorities

• Volatility due to commodity price dependencies

• Geography e.g. infrastructure challenges, difficult topography

• Scale e.g. many rather small markets

The key to mastering these challenges in LATAM lie in the distribution network. If companies can strip away the layers of complexity in distribution, they have the potential to reduce costs, streamline their processes and implement more customer-centric service offerings.

Decisions LSH companies have to take in LATAM around distribution

When devising a distribution strategy in LATAM, LSH companies have to consider multiple questions.

- Where to keep inventory in the region, in which country or whether to use regional inventory in a free trade zone?

- Should their business units’ products be distributed separately or in a joint consolidated distribution network?

- Should they operate their own warehouses or rely on logistics service provider run warehouses or stay out of the country all together and rely solely on distributors?

- From which locations and with which providers can direct-to-patient shipments be offered?

How LSH companies are currently distributing in LATAM

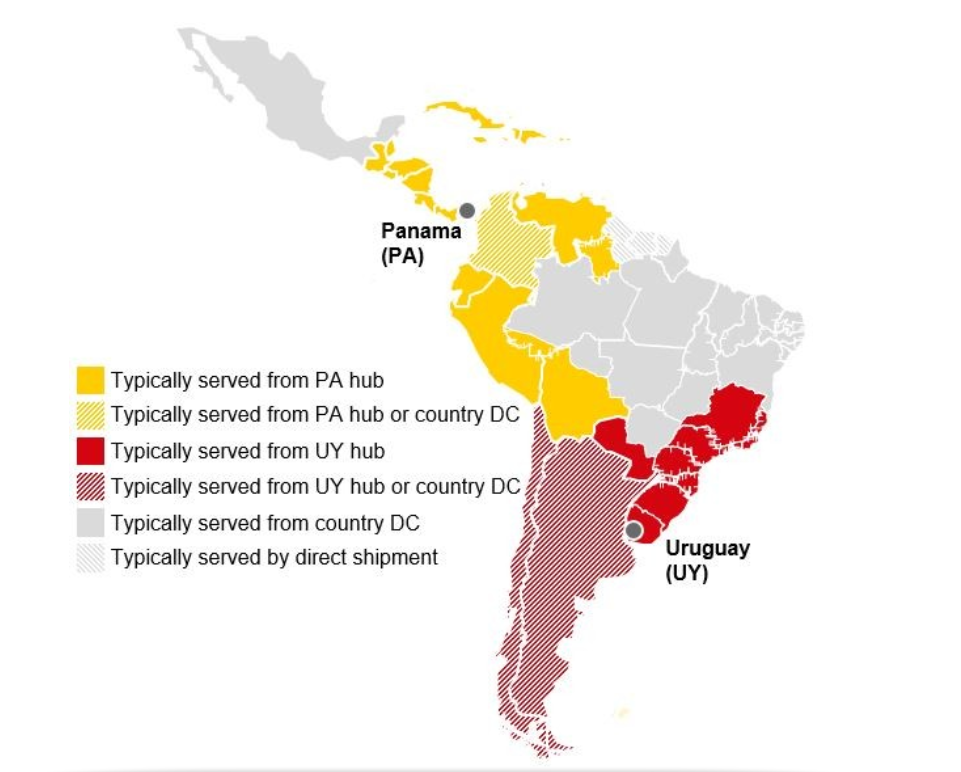

As of now, most companies manage distribution in large markets, such as Brazil, Mexico, Argentina, Chile and Colombia from owned or outsourced warehouses within the countries themselves.

Smaller countries are served either from a regional warehouse to distributors (e.g. Central America) or via direct shipments from manufacturing origin to distributors in South America (e.g. Paraguay, Bolivia). On average, LSH companies have inventory in 10 warehouses in LATAM with the vast majority of their warehouses being outsourced to logistics service providers.

Most LSH companies also have one regional warehouse in a free trade zone, to serve as a hub, mostly Panama for Central America and Caribbean (although other locations in Central America are also used for legacy reasons) and Uruguay for the southern cone and some southern Brazilian states.

Changing distribution requirements are impossible to achieve with status quo

LSH companies are increasingly interested in offering direct-to-patient shipments for various reasons such as bypassing distributors, accounting for new personalized medicine requirements or offering compassionate use drugs. However, the above status quo makes implementing such services difficult.

Logistics service providers in LATAM are ready to offer direct-to-patient shipping, as the processes do not differ from other industries’ clients established processes (e.g. Technology). However, direct-to-patient shipping from a regional warehouse can still take a long time due to health authority clearance times, and be complex due to prescription requirements. In some cases, LSH companies are tied up in long-term distributor contracts that do not allow for a second direct distribution channel.

How LSH companies should prepare for future LATAM distribution

To succeed in implementing a distribution network in LATAM that has the agility to keep up with future developments in medical technology and increasing customer expectation, companies should examine if a hub in a free trade zone could result in cost benefits, better market access and reduced complexity for them. LSH companies that find a hub in a trade free zone to be a viable solution for them, usually benefit from:

- Transport consolidation and transport mode shift benefits (air to ocean) on the inbound

- Demand peak smoothing effects when late stage labeling for each local market is applied

- Lead time reduction on the outbound (in case of direct-to-patient shipments)

- Inventory carrying cost reduction

- Duty payment deferral benefits

When thinking about a hub LSH companies should be aware of the following:

- Panama and Uruguay complement each other as hub locations given their favorable free trade zone legislation, superior infrastructure, stable political and economic environment and logistics service provider presence

- Their coverage does not overlap and together spans all of LATAMs markets

- While Panama is widely known as a hub location, Uruguay’s potential is not as well known yet, but equally proven to meet the needs of the LSH industry

To evaluate the potential of a hub, supply chain executives should conduct rigorous end-to-end cost component analysis including inbound and outbound transport, warehousing, inventory carrying and management costs as well as duty / tax implications. This analysis will prepare them to answer their business units’ likely questions around a hub’s compliant airlift capacity, secure road connectivity, customs clearance processes, transit time and cost implications.

Conclusion

LSH companies that can successfully manage the transition from legacy grown distribution structures in LATAM to more flexible, less complex ones, that allow them to implement customer centric, personalized healthcare solutions will find themselves at a huge advantage. By taking steps to make this transition now they will be able to build trust and establish themselves as leaders in the industry.

For complete article: https://www.linkedin.com/pulse/meeting-new-market-requirements-life-sciences-latin-america-behncke/?trackingId=hbinrZSHRRSGCNSFYhCR8A%3D%3D17:02